Human Health

Biological Awareness

The most obvious characteristic of science is its application, the fact that as a consequence of science one has a power to do things.

Richard Feynman, 1963

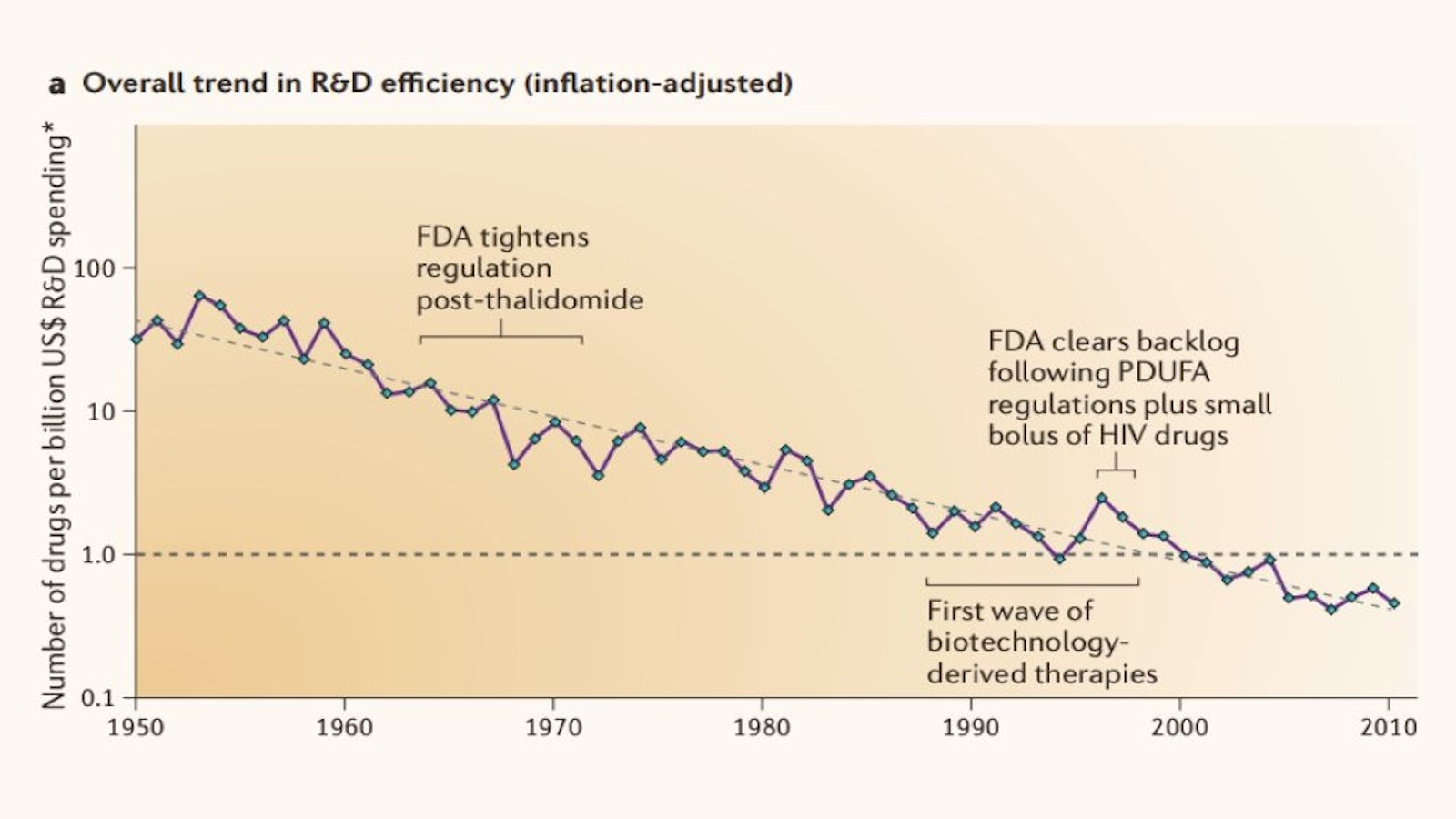

A lot can happen in a decade, and a lot has. At Obvious, 2026 marks ten years of investing at the intersection of frontier AI and the life sciences. What used to be a liminal space has now transformed into one the most promising areas of AI. Our journey in this field began with a curiosity that had yet to crystalize into a full thesis: Could AI stem or even reverse the secular decline in productivity in making medicines, as described by Eroom’s Law,1 within one of the world’s most positive-externality-producing industries?2 (The short answer: it most certainly, will.)

Since then, this field has undergone a rapid pace of progress. Most technology primitives have been fully overhauled. Our first portfolio companies such as Recursion and Dyno Therapeutics were early in training convolutional neural networks for phenotypic screening and recurrent neural networks for AAV capsid design, respectively, while LabGenius Therapeutics was among the first companies to use multi-objective Bayesian optimization to compose bi-specific T-cell engagers. Nowadays, the dominant paradigm is to train large biological foundation (and more recently) world models. Unsurprising to us, the visionary and resourceful founders of these founding era companies always manage to embrace novel technologies and partner with the right groups to stay one step ahead. A great example of this is Recursion’s collaboration with our friends at Boltz on the breakout release of Boltz-2 last year, the most open competitive protein structure and molecular interaction model last year,3 and Dyno’s model evaluation collaboration on Anthropic’s Mythos model4 and OpenAI’s GPT-Rosalind5 earlier this year.

Category names have shifted with equal restlessness. What was once called CompBio became TechBio, the standard banner of the community for about half a decade. However, recently a few category names, like AI × Bio, BioAI, AI4Science, have been proposed to signify the post-Transformer and post-AlphaFold moment we are in. We humbly suggested Generative Science.6

This piece cannot cover everything that happened in these years but the shortest faithful approximation of the major events that shaped the past 10 years is as follows:

- The first generation of TechBio companies piqued investors’ interest in backing medicine-making companies predicated on large-scale, industrialized data generation paired with (at the time only weakly capable) machine learning models. This was an alternative to the then-dominant mode of funding companies that relied on artisanally gained biological insights – often during a founders PhD or post-doc – in an increasingly virtual biotech mold.7

- COVID accelerated the development and worldwide deployment of mRNA vaccines, a technology we believe would otherwise still have been languishing in clinical trials. The pandemic also led to the rapid rise of two platform companies, Moderna and BioNTech SE, whose products saved countless lives and market capitalizations rose to a combined all-time high of $275 billion.

(As a side note: mRNA vaccines are a great starting point, but the real promise of AI lies in its potential to design any sequence-based medicine with superior properties across many different modalities and delivery mechanisms. After seeing some of Inceptive‘s internal model capabilities, we believe that a breakthrough moment is coming before the end of 2026.)

The pandemic was also a harbinger of the supply chain dependencies and geopolitical decoupling that are about to come (more on this in our section on the BIOSECURE act).

- AlphaFold’s victory at CASP14 was the right evocative problem to solve. Similar to AlphaGo’s win against Grandmaster Lee Sedol in Go, Demis and the Google DeepMind team again picked the right problem to solve and inspire awe in the broad public. Thanks to AlphaFold, this entire field of Generative Science has been imbued with massive societal goodwill.

This is, perhaps, not an entirely immaterial reason for the frontier AI labs to pursue breakthroughs in biology. In addition, of course, there is a sizably large economic opportunity: biopharma represents roughly 9% of the S&P 500, or about 14% of the index after excluding technology and energy companies.8

Where do we go from here?

If the next decade of Generative Science unfolds with similar twists, turns, and accelerations, it promises to be an extraordinary time. Below are a few ideas – some near-term, operating on several months timescale, others macro, playing out over multiple years – that we are thinking about (shorthand for: areas in which we would like to invest).

Task-specific experimental tokens are the new gold in biology

Scaling laws are weirdly shaped in biology. They do sometimes exist in almost pure form. Eric Nguyen and colleagues’ work on the Evo models – a genomic foundation model trained on 2.7 million prokaryotic and phage genomes at single-nucleotide resolution – demonstrated that one could predict the functional consequences of DNA mutations across the tree of life with no task-specific supervision whatsoever. Emergent capabilities, like zero-shot function prediction, and multimodal generation (DNA, RNA, proteins) that are enabled by scale and are on par or beat hand-tuned models for specific tasks is the closest we have to scaling laws in language.

However, the pure-form scaling laws seem to be an exception rather than the rule. Empirically, we see the winning factors for model performance have more often been experimentally generated, task-specific tokens. This more specialised training data acts as jet fuel, allowing small teams that are compute-constrained to outperform large frontier labs on highly valuable modelling tasks. The pattern holds across the complexity spectrum of medicines, from small molecules to the most advanced biologics formats. Take the following two examples:

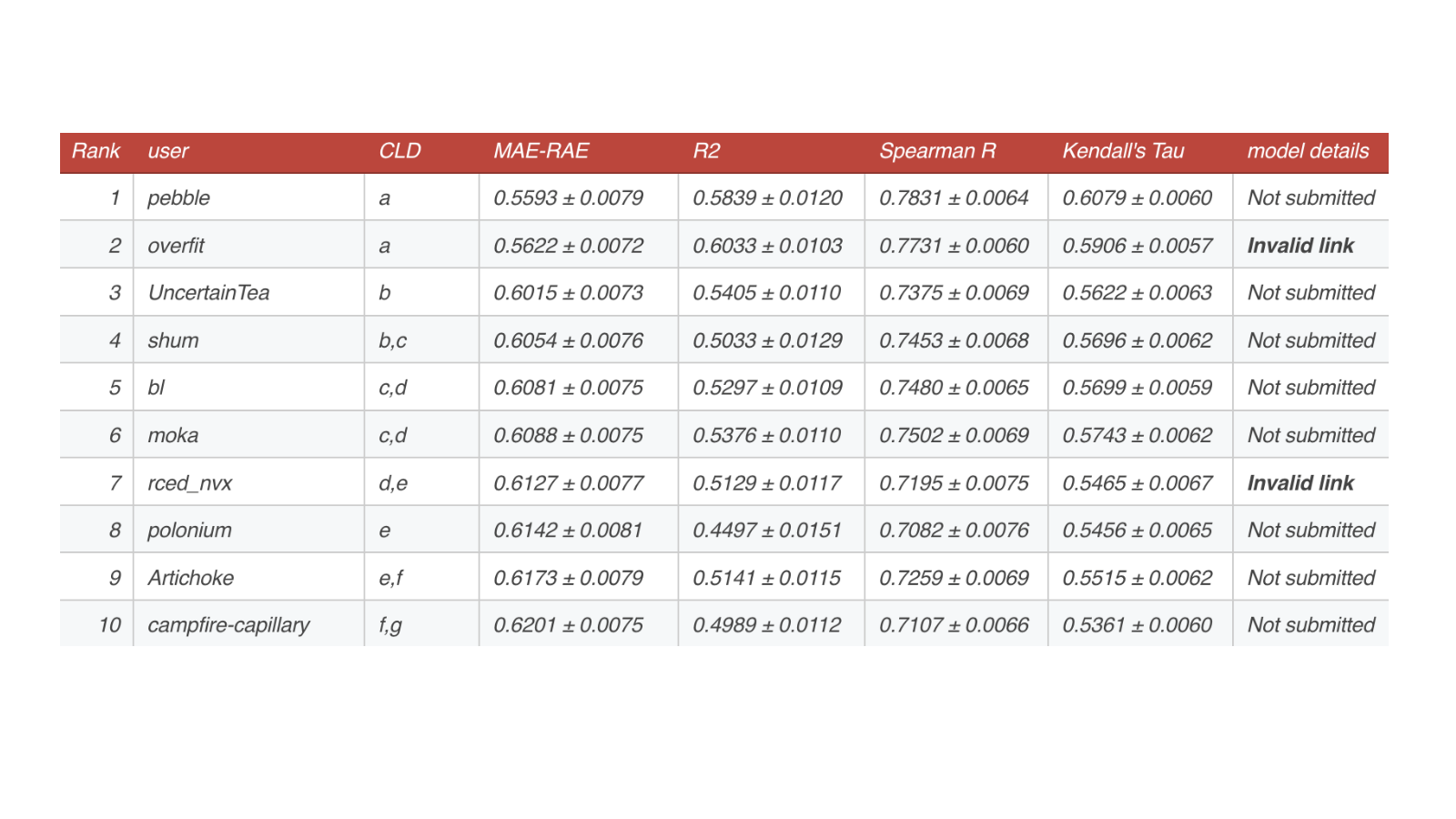

Inductive Bio is solving ADMET – Absorption, Distribution, Metabolism, Excretion, and Toxicity – a canonical task for the optimization of important drug properties. They focus on small molecules which remain the mainstay of the pharmaceutical industry (roughly 60-70% of new FDA-approved drugs in recent years have been small-molecule drugs). In this field, the Inductive team recently won the OpenADMET-ExpansionRx blind challenge, the largest competition of its kind, placing first among more than 370 submissions, ahead of teams from the biggest pharmaceutical companies like Merck, EMD Serono, Inc. and also frontier AI companies, like NVIDIA.10 Inductive’s key advantage cannot be attributed to more GPU-hours or model parameters. It lies in a unique pre-competitive data consortium of biotech companies that cumulatively have contributed more than a billion experimental chemistry tokens. The more nuanced point is that this consortium data samples far more interesting and diverse regions of the chemical universe than any single large pharma company’s archive could. Combining a compounding token advantage with an intelligent use of expert feedback and reinforcement learning is what led to state-of-the-art performance.

If small molecules are the oldest, most battle-tested form of modern medicine, T-cell receptor-based (TCR) therapies sit at the other extreme, among the most cutting-edge interventions in the pharmacopoeia. They offer an unprecedented advantage in their specificity but TCRs so far have only been able to be screened from human blood, making it impossible to find near-optimal TCRs in a 10^24 combinatorial space. Two approved drugs have been created through the screening approach,12 but computational design has eluded this field thus far because general protein models can (among other things) not design hypervariable and conformationally flexible loops against a composite (peptide-HLA) ligand well. Synteny is solving TCR design by building AI models to recapitulate the underlying biology of how TCRs bind to antigens and activate the immune system, a holy grail problem. The company is getting tantalizingly close to declaring victory, through their first fully de novo designed TCR bispecific against one of the hardest cancer targets. And again, success here is not only a matter of competence across protein language models, diffusion and energy-based models—though Synteny uses all of these model types—but of doggedly building a highly proprietary assay cascade and data generation engine that has yielded roughly a 1,000x larger in positive TCR-binding data set compared to the entirety of the public domain, and a 100,000x increase in negative binding pair tokens, according to Synteny internal data. Go figure: negative examples are valuable tokens too when teaching machines TCR biology.

Where does that leave us?

About three years ago, there was a vocal camp in the field insisting that the public domain already contained all the biological data anyone could need, that the bottleneck was algorithms and compute, not experimental tokens, and that the right architecture applied to existing datasets would be sufficient to crack the hardest problems in drug discovery and molecular biology. Even the most vocal among them have since fallen silent, and some are now quietly purchasing bespoke data to move their platforms and programs forward. Which leads us to our second idea.

Bio AI data factories will pioneer a new business model for selling experimental tokens

While most of the AI infrastructure is being solved horizontally, data generation has to be vertical in biology. Our Generative Science companies are competing for the same GPUs as other non-bio frontier labs, but they are not buying data from Scale, Mercor, and Surge AI, at least not yet.

Vertical data-generation companies that power large-scale model development will become a defining category in biology. Robotics offers an instructive case study of a field that is, we believe, roughly 12 to 18 months ahead of biology in this regard. The race to generate the most compelling corpora of simulation or teleoperation data – be it exocentric, egocentric, or multi-view – is in full swing. Some frontier robotics labs are generating data in-house (not much different from the initial TechBio approach), and some are buying data from specialized providers like XDOF. Some of those data providers, in turn, harbour ambitions of building their own frontier models. There is a physical instantiation of this bio AI data factory that looks remarkably close to robotics data generation. Medra has done impressive work rapidly standing up robotic arms and training those in a laboratory environment (video).

We may be biased here, but data generation in biology requires much more tacit knowledge handling finicky high-end lab instruments,14 parsing ambiguous protocols, managing ambient conditions and seems overall to be harder than robotics data generation. The sweet spot for a bio AI data factory is a Goldilocks zone: being able to rapidly industrialise data-generation output measured on a log scale (not in percentages) while also tightly coupling the type of data – that is, the type of assays – to where the leading edge in bio AI actually sits.

Right now, that leading edge is kinetics data: the binding curves and molecular interaction behaviours that teach models not just whether two molecules interact but how (how fast, how tight, how reversibly). Adaptyv opened the market through providing simple API-first for protein synthesis and validation jobs. Our friends at Instance are about to set the new standard when it comes to scaled up data generation for model training and inference-time steering.

None of the above is going to meaningfully change the industry’s composition anytime soon. Our prediction is that zero out of the top twenty pharma companies will be AI-native within the next five years; ten years from now is a whole other story. Prioritizing the productization of frontier AI within large pharma enterprises is therefore of utmost importance.

Smoothing out the jagged frontier for pharma enterprises is where fortunes will be made

Drug discovery will not be monolithically dominated by one foundation model. Ergo, the proper orchestration of workloads across the most capable models – and suffusing those models with the appropriate context – is critically important to realizing real-world productivity improvements from target identification through molecule design and optimization, pre-clinical testing, and of course beyond the discovery stage.

Mithrl is laser focused on smoothing out this jagged frontier. Their scientific decision engine is a harness that runs more than 150 sub-agents on top of large frontier models, open-source models, and custom client models. It continuously evaluates the right models for the right tasks and ensures that every decision and analysis is accurate, reproducible, and transparent to cross-functional discovery teams. This allows Mithrl to abstract away the complexity for its partners, which include some of the largest pharma enterprises, among them Johnson & Johnson and Roche.

Ultimately, the layer that will prove necessary is one that understands scientific intent, acts as an arbiter of model quality for specific tasks, and integrates a pharma company’s proprietary in-house models into the broader orchestration. Going the extra mile here means blurring the lines between software platforms and service models. Perhaps Forward Deployed Scientists will become a hot job category among biology PhDs.

If you have read this far, you might reasonably ask: but what about clinical development, the business of running clinical trials to generate human data? That is, by any honest accounting, the most expensive and protracted stage in the entire arc of bringing a medicine to market. Our possibly controversial take is, due to the impedance mismatch between rapid speed of technology development but the glacial pace of procurement and adoption cycles within large pharma enterprises, we will first see clinical trial intelligence breakout in the financial realm first.

Clinical trial intelligence will be financialized before it is operationalized

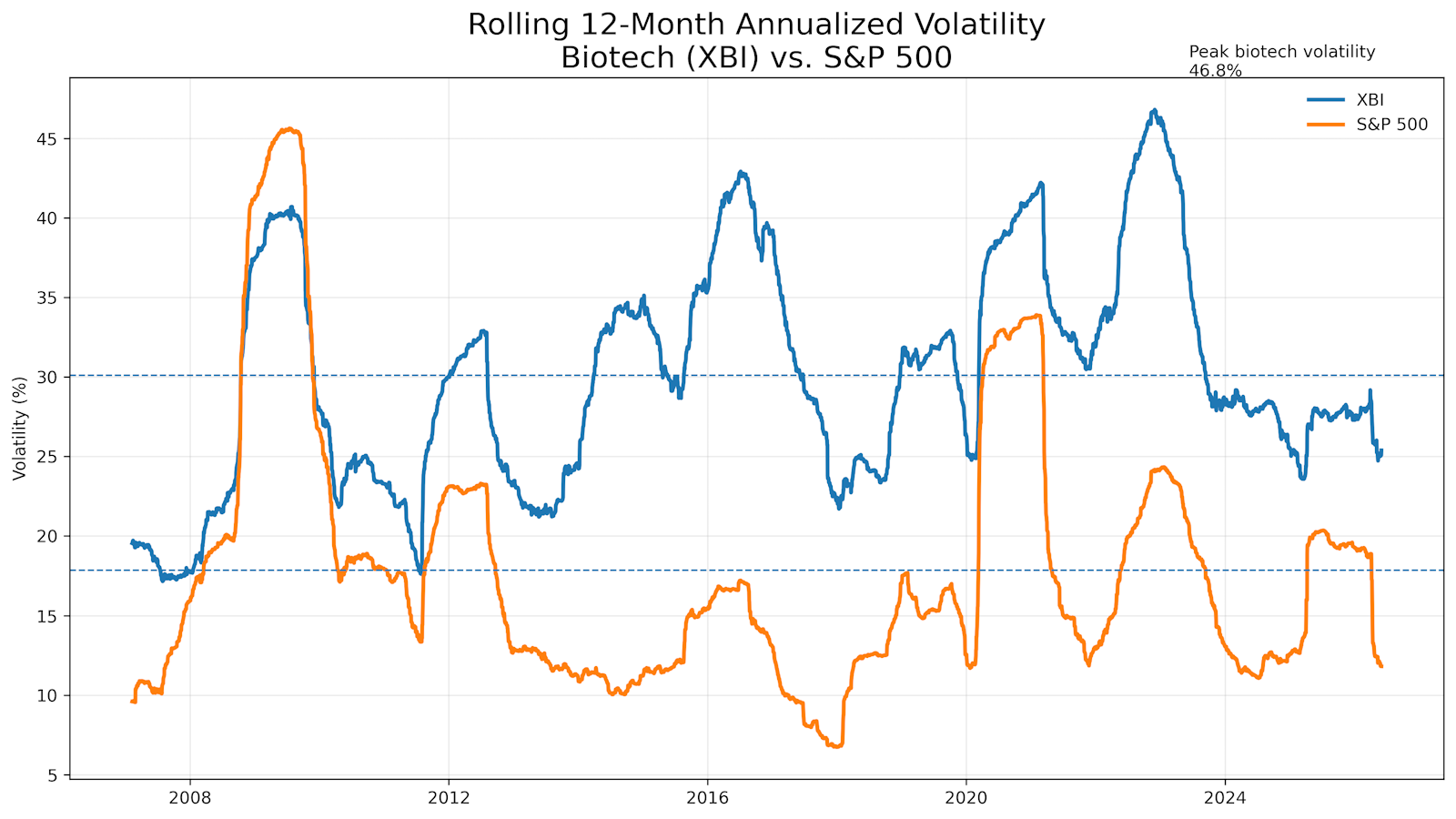

Predicting the outcome of a clinical trial is, perhaps, the single most lucrative task in all of biopharma. From a financial vantage, drug development resembles a long sequence of binary (perhaps weighted) coin flips. Does the candidate clear IND-enabling studies and enter the clinic? Does the program meet its endpoints in clinical studies? What will the FDA’s advisory committee recommend? Each flip has staggering implications. A positive readout from a pivotal trial can conjure billions of dollars in enterprise value while a negative readout can send biotechs into bankruptcy. At an individual company or program-level, the system is non-ergodic.15 Non-ergodicity combined with the peculiar construction of the premier biotech stock index, SPDR S&P Biotech ETF (XBI), which is equally weighted between small single-program companies and revenue-producing, well-diversified pharmaceutical companies and industry-wide correlation, creates extraordinary volatility on an index basis too. Over the past two decades, the XBI has exhibited annualized volatility in the range of 30%, nearly double the roughly 15% for the S&P 500.16 Volatility is a feature and not a bug if you can trade on it.

It becomes readily apparent, then, that the first and most aggressive deployment of clinical trial intelligence will be financial rather than operational. New AI-native biotech hedge funds will be established that build their own language models and agentic workflows. Their work will be to ingest the world’s scientific literature, read financial reports and expert call transcripts, and parse regulatory filings. These hedge funds will also rely on novel alternative data sources, such as full regulatory dossiers of the bankruptcy mass of defunct biotechs – a practice that has been proven out by the Renaissance Philanthropy-backed CTD Commons Fund – or integrating signals from prediction markets like Kalshi.17 We are excited to see what the teams at Abundance and 76th Street Research will launch.

While AI will change public biotech investing wholesale in a very short amount of time, its impact on improving operational efficiency of clinical trials will be substantial but more piecemeal at the outset. Many discreet clinical trial processes already have best-in-breed AI solutions, like protocol authoring and design by Faro, and some pharma companies are also building their in-house modules by partnering with large frontier labs.

However, the operational complexity – some suggest that there are multiple thousands of processes involved in running trials across the sponsors, sites and patients – means in order to drive very large efficiency gains one might either have to co-own the site of research, like Iterative Health’s model, or build an entirely clinical trials operating system from scratch like Pi Health does. Pi Health’s tabula rasa approach has the chance to rectify the original sin in this space, namely the lack of unified database and hyper-fragmentation of modules and vendors. Instead of, metaphorically speaking, pitching the circus tent anew for each new trial, could a clinical research coordinator or associate (and in the future their respective agents) run trials on a single system, reducing the need for custom integrations and consultative services? As writing code becomes cheaper thanks to technologies like Cursor and OpenHands, the regulatory overhang caused by outdated compliance and validation frameworks, such as GxP requirements will remain the bottleneck. The totality of the number of test cases, often multiple thousands, and validations documents, many hundreds, to build a clinical trials operating system are truly staggering. This is the natural speed limit.

The above example illustrates that regulatory innovation is at least as important as new technology for improving clinical trials operations. We are hopeful to see movement and new ideas from regulators, such as FDA’s pilot programs on real-time clinical trials, that could have a positive impact.18

In our most utopian view, better capital allocation to the right trials and increased efficiency running these running trials could make a big dent in reversing Eroom’s law.

Up to this point, this article has discussed the bull case for Generative Science. We must also review the alternative possibilities, namely the potential for AI in biology to cause catastrophic harm.

The bioweapons threat is real, it is accelerating, and has not been sufficiently priced in

When some of the sharpest minds in AI safety rank biothreats at or near the top of their p(doom) ledger,19 it is time to pay attention.

Daniel Kokotajlo et al’s essay AI 2027 describes a fictional but scary scenario in which a misaligned superhuman AI secretly designs a super bioweapon that ends the world as we know it.20 But we don’t even have to go that far to find potential for real-world harm that is caused by leveraging AI to design biothreats. Jonas Sandbrink laid out a good framework to distinguish between: i) using general LLMs to lower the barrier to design and produce known threats by possibly individual actors; and ii) the scenario where nationstates or other well-resourced groups could use bio-design tools (think: very capable, specialized models) to design novel threats.21

The evidence for the former scenario was mixed at the beginning. In 2024, a study on OpenAI concluded together with Gryphon Scientific that there was no meaningful uplift for novices to design biothreats using GPT-4.22 Since then, a 2025 OpenAI study concluded that Deep Research “can help experts with operational planning to reproduce biological threats.” Later on, the o3 and o4 systems cards stated that these models were more skilled in answering questions for biothreat creation. The ChatGPT agent system card classifies agents as highly bio-capable, introducing new safety concerns.23 A similarly concerning trajectory was found at Anthropic with perhaps the escalation point reached in the 2025 Claude Opus 4 expert uplift study, which found that participants using Claude made far fewer mistakes in developing biothreats compared to an internet only group.24 This triggered Anthropics Safety Level-3, a threshold which signifies that potentially meaningful uplift for someone trying to create bio weapons could be provided. General models are becoming increasingly capable of lowering the barriers for novices to re-produce existing bio weapons.

Now, let’s look at the second question: can specialized bio-design tools create novel threats? The short and sobering answer is yes. In 2022, at a Swiss security conference, computational chemists (not AI researchers) re-purposed MegaSyn, an older AI tool for small molecule design, by inverting its objective function to create nerve toxins. In six hours, they created 40,000 novel compounds with many of them predicted to be more toxic than VX, a compound where a single drop could be lethal.25

In summarium, models are getting more capable at lowering barriers and raising ceilings of biothreats. The means of production, in many cases nucleotide synthesis is far from adequately protected26 and might even become more decentralized and is therefore harder to safeguard. Additionally, history is proof that some of the most well-resourced actors, nation states, have and (potentially are) pursuing large-scale bioweapons programs.27 This is a perfect storm brewing that could lead to bad outcomes.

It’s time to prepare for this eventually. At Obvious, we are proud to have backed leading AI researchers who are building a bio AI lab with a dual mandate: to develop both leading biological interventions to prolong life and capabilities to protect life from bioweapons (soon to be announced). We are also actively looking for teams building the KYC-layer to steward access to frontier intelligence while denying catastrophic harm. We think trusted access needs to be co-owned by a third party that can coordinate across frontier models and labs.

None of these things in isolation are absolute guarantees to prevent harm, but together they can meaningfully lower p(doom).

Let’s move on from biosecurity to the BIOSECURE Act. A piece of legislation that, in our opinion, is widely under-discussed.

The BIOSECURE Act will fundamentally reshape supply chains

As we near the Thucydides trap with China, we will see critical industry decoupling – first slowly, then very fast.

China has risen as a biotech leader. Over the last few years, Chinese assets in 2025 have accounted for 28% of all active innovative programs in clinical pipelines, up from 14% in 2020 and 4% in 2015.28 Chinese assets accounted for $138B of total deal value – or, put differently, one-third of all cross-border licensing deals in biopharma.29 The cost advantage and speed of discovery and early-stage clinical development is significant.

While commercial activity between leading Western biopharma companies and Chinese biotechs is increasing, the winds at a policy level, and especially the discussion around securing critical supply chains and national competitiveness, are blowing in a different direction. In December 2025, after several failed attempts, core components of the BIOSECURE Act passed as part of the defense spending bill.30 The BIOSECURE Act aims to ban federal agencies and private companies that receive federal funds from working with “biotechnology companies of concern.” The list of companies of concern will be published by the end of this year and is widely expected to include five Chinese companies: WuXi Biologics, WuXi AppTec, BGI, MGI Tech, and Complete Genomics, all of which were directly named in previous drafts of the act.

If national alternatives are not built in time, the supply chain disruption caused by the BIOSECURE Act would make US biotechs scramble. Consider the chemistry work that goes into optimizing a small molecule program and bringing it into the clinic. This is a labor-intensive process: medicinal chemists often design hundreds and sometimes thousands of molecular permutations and synthetic chemists, then attempt to make and test them. In aggregate, we think roughly 80% of this work for US biotechs goes to WuXi AppTec and Pharmaron, the two premier Chinese suppliers. These two companies enjoy large labor advantages: Pharmaron and WuXi employ more than double the number of chemists (about 30,000) than the entire use US biopharma industry taken together (about 14,000)31 at around 64% lower cost.32 Ironically, the third largest player in this space, Enamine Ltd. , is a Ukrainian company that did a valiant job ensuring continuity of operations when its main site in Kyiv was under threat during the Russia-Ukraine conflict, but it is fair to say that this supply chain is tenuous at best.

So how does one rebuild this supply chain in the US? Not through identical replication. In the case of small molecule chemistry, there are simply not enough chemists in the country. It has to start with AI and thoughtful automation at each step of the process. AI platforms like the one Inductive has built have repeatedly optimised the chemical properties of molecules that made it into the clinic with 50% fewer designs needing to be synthesised and tested, and in half the time. Better molecule optimisation combined with increasingly automated synthesis means fewer US chemists could do better and faster work in designing medicines that reach the clinic.

As we can now see, geopolitics will spur major upheavals in the pharma supply chains, but they can only be reimagined through extensive use of AI.

The best way to predict the future is to invent it.

Alan Kay, 1971

Closing Thoughts

The next decade in Generative Science promises to be exhilarating thanks to AI. We have touched on a few themes here and omitted many others, from space biomanufacturing to protein sequencing to artificial wombs. With a measure of luck and a great deal of determination, an era of abundance powered by AI-enabled biological breakthroughs may be within our grasp. If you are building this future, we would like to hear from you.

Notes & Citations

[1] Jack W. Scannell, Alex Blanckley, Helen Boldon, and Brian Warrington, “Diagnosing the Decline in Pharmaceutical R&D Efficiency” (2012). The authors coined the term Eroom’s Law (“Moore” spelled backward) to describe the long-term decline in pharmaceutical R&D productivity despite advances in science and technology.

[2] Peter Kolchinsky, The Great American Drug Deal (2020). Kolchinsky argues that paying for patented medicines is analogous to paying a mortgage: society bears the upfront cost during the exclusivity period, but once patent protection expires, the innovation effectively becomes a public asset that can generate benefits indefinitely.

[3] MIT and Recursion, Boltz-2: A Next-Generation Open Model for Biomolecular Interaction Prediction (2025). The release of Boltz-2 marked a significant advance in open-source biological foundation models, providing model weights, inference code, training data, and state-of-the-art performance on protein structure and molecular interaction prediction tasks. Recursion collaborated with researchers at MIT and the Boltz team to help develop and release the model.

[4] Anthropic, Mythos Preview System Card (2026). Mythos is Anthropic’s biology-focused AI model, developed to support reasoning and prediction tasks across molecular biology and drug discovery. Dyno Therapeutics collaborated with Anthropic on model evaluation efforts to assess performance on biologically relevant design and prediction tasks.

[5] OpenAI, Introducing GPT-Rosalind (2026). GPT-Rosalind is OpenAI’s frontier model for biological research and drug discovery. Dyno Therapeutics participated in external evaluation efforts, helping assess the model’s capabilities on real-world biological design challenges, including tasks relevant to gene delivery and protein engineering.

[6] Obvious Ventures, Generative Science: Our Contrarian View of AI (2024). In response to the proliferation of labels such as TechBio, AI × Bio, BioAI, and AI4Science, we proposed the term Generative Science to describe the emerging convergence of foundation models, scientific discovery, and experimental validation. The term reflects our view that AI’s most profound impact on biology will come not from automating existing workflows, but from expanding humanity’s capacity to generate new scientific knowledge.

[7] The “virtual biotech” model emerged in the 2000s and 2010s as a capital-efficient approach to company creation, in which small teams advanced drug programs by outsourcing much of the underlying research and development infrastructure. See Jonathan Montagu’s writings on LifeSciVC (2014) for a contemporary discussion of the model. To be clear, we remain enthusiastic about the virtual biotech approach and are excited by the possibility that AI could further compress organizational requirements, enabling what Zak Doric, PhD has described as the first true “one-person biotech.”

[8] Internal Obvious analysis of S&P 500 constituent market capitalizations. We estimate that publicly traded biopharma companies account for approximately 9% of total index value. Technology and energy companies account for roughly 35% and 3% of the index, respectively. Excluding those sectors leaves biopharma representing approximately 14.5% of the remaining index by market capitalization.

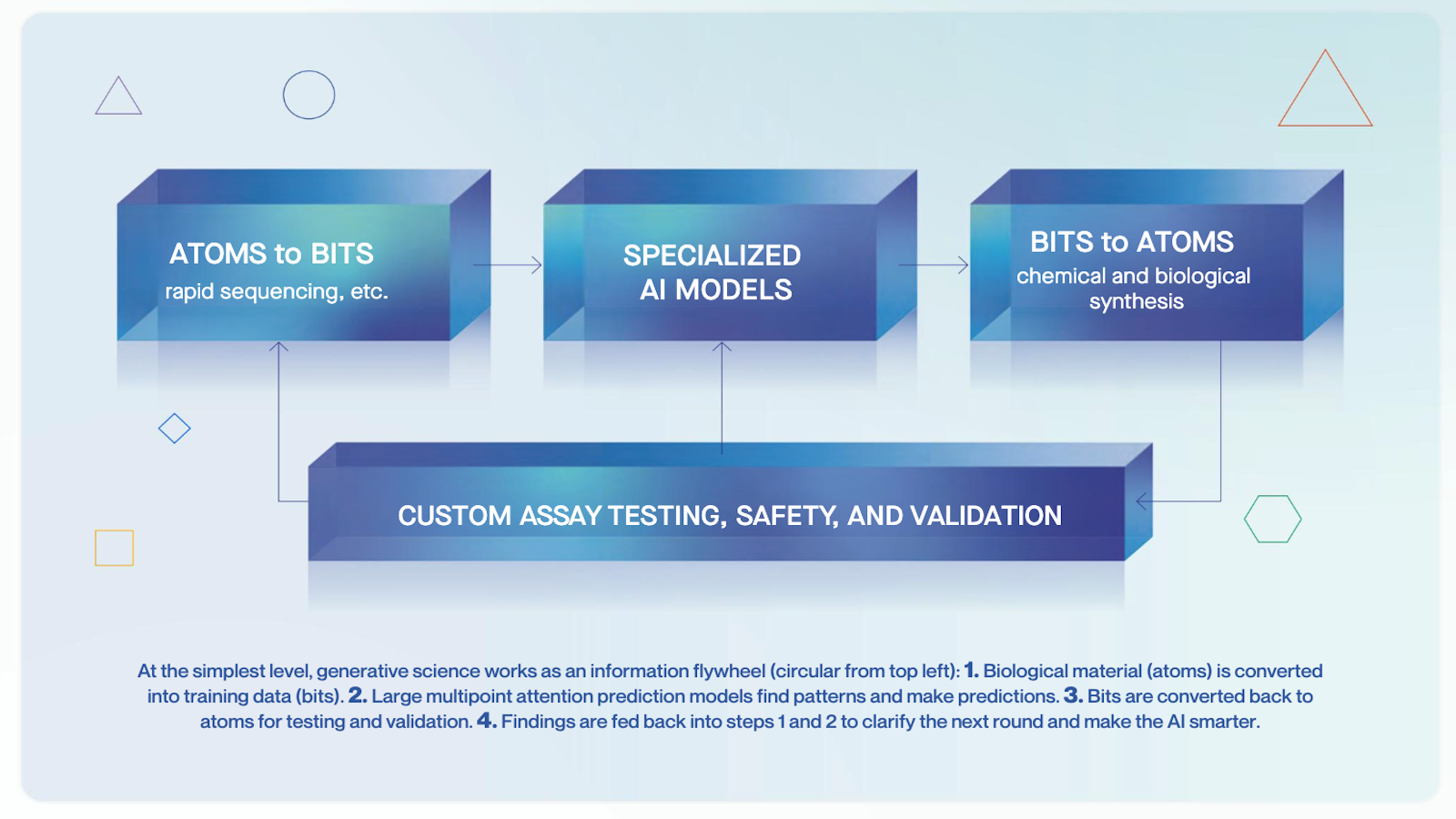

[9] Obvious Ventures, World Positive Report 2025. The Generative Science Flywheel illustrates how advances in AI and experimental biology reinforce one another through a continuous feedback loop of data generation, model development, and scientific discovery.

[10] Inductive Bio, Inductive Bio Wins World’s Largest ADMET Prediction Competition, Advancing the State of the Art in Real-World Drug Discovery AI (2026). Inductive’s Beacon models placed first among more than 370 submissions in the OpenADMET-ExpansionRx blind challenge, outperforming teams from large pharmaceutical companies, biotech firms, academic institutions, and AI organizations.

[11] OpenADMET Consortium, OpenADMET-ExpansionRx Blind Challenge Results (2026). The challenge attracted more than 370 submissions from participants across industry, academia, and AI research. Inductive Bio’s submission (alias “pebble”) ranked first on the final leaderboard.

[12] Two T-cell receptor (TCR)-based therapies have received regulatory approval to date. KIMMTRAK (TCR bispecific) was first approved in 2022 for metastatic uveal melanoma and TECELCRA (TCR-engineered T cell therapy) was first approved in 2024 for metastatic synovial sarcoma.

[13] Medra, Introducing Medra Lab 001 (YouTube, 2026). The video introduces Medra Lab 001 (ML001), a 38,000-square-foot autonomous laboratory designed to support AI-driven scientific discovery through large-scale experimentation, robotics, and continuous data generation.

[14] Author observation. In our experience, almost every AI biology company that has built high-throughput, experimentally complex assays eventually discovers how temperamental laboratory automation can be. Whether working with Carterra platforms for antibody screening or Miltenyi Biotec systems for cell therapies, changes that appear straightforward on paper often require extensive troubleshooting, optimization, and domain expertise in practice.

[15] Non-ergodicity in this context means that even if drug discovery as a whole has a positive expected value (ensemble average), no single company can achieve the ensemble average due to the binary risk of failure mode in clinical trials (time average for a single participant). To clarify, some companies can exceed the ensemble average materially by producing blockbuster drugs through clearing multiple, sequential binary bets (clinical trials).

[16] Obvious analysis of historical daily price data for the SPDR S&P Biotech ETF (XBI) and the SPDR S&P 500 ETF Trust (SPY), sourced from Yahoo Finance. The chart shows rolling 12-month annualized volatility calculated from daily returns. XBI has exhibited substantially higher volatility than the broader market over most of its history, reflecting the binary outcomes and concentrated risk characteristic of biotechnology investing. Data retrieved from Yahoo Finance historical price series for XBI and SPY.

[17] Kalshi offered a market on whether Eli Lilly’s retatrutide would receive FDA approval before January 2027. At the time of writing, one could potentially make $1.82 for each $1 bet on the affirmative. While far from perfect, prediction markets can serve as a valuable source of probabilistic information, aggregating dispersed knowledge about binary events such as clinical trial readouts and regulatory decisions.

[18] U.S. Food and Drug Administration, FDA Announces Major Steps to Implement Real-Time Clinical Trials (2026). The FDA launched proof-of-concept real-time clinical trials with AstraZeneca and Amgen and issued a request for information for a broader pilot program. The initiative aims to enable regulators to monitor safety signals and clinical endpoints as they emerge rather than waiting for traditional reporting cycles, with the goal of accelerating drug development and improving trial efficiency.

[19] P(doom) is AI safety shorthand for the probability that advanced AI systems ultimately cause an existential catastrophe or irreversible civilizational collapse.

[20] Daniel Kokotajlo et al., AI 2027 (2025). The essay presents a fictional scenario charting the development of increasingly capable AI systems and explores several catastrophic risk pathways.

[21] Jonas Sandbrink, Artificial Intelligence and Biological Misuse: Differentiating Risks of Language Models and Biological Design Tools (2023). The paper is notable for moving the debate beyond the simple question of whether AI increases biological risk. Instead, it provides a framework for assessing which capabilities matter, who is likely to gain access to them, and how those factors influence overall threat levels.

[22] OpenAI and Gryphon Scientific, Building an Early Warning System for LLM-Aided Biological Threat Creation (2024). In a controlled study, researchers found that access to GPT-4 did not meaningfully increase novices’ ability to create biological threats.

[23] OpenAI, Deep Research System Card (2025); o3 and o4-mini System Card (2025); and ChatGPT Agent System Card (2025). Across successive evaluations, OpenAI reported increasing biological capabilities in its frontier systems, including assistance with operational planning, stronger performance on biothreat-relevant questions, and agentic behaviors that introduce new biosecurity considerations.

[24] Anthropic, Claude Opus 4 Expert Uplift Study (2025). The study reported that experts assisted by Claude Opus 4 made substantially fewer mistakes on biothreat-relevant tasks than an internet-only control group, suggesting meaningful capability uplift for knowledgeable users.

[25] Urbina et al., Dual Use of Artificial Intelligence-Powered Drug Discovery (2022). Researchers demonstrated that an AI system originally developed for therapeutic small-molecule discovery could be repurposed to optimize for toxicity rather than safety. In a proof-of-concept exercise, the model generated tens of thousands of potentially hazardous compounds, illustrating how biological and chemical design tools can be redirected toward harmful objectives with relatively minor modifications.

[26] Bruce J. Wittmann et al., Strengthening nucleic acid biosecurity screening against generative protein design tools (2025). The authors, including Microsoft Chief Scientific Officer Eric Horvitz, demonstrated that AI-generated variants of known protein toxins, including ricin, were not detected by the sequence-screening systems of leading DNA synthesis providers such as IDT and Twist.

[27] Ken Alibek, Biohazard (2000). Alibek, a senior scientist in the Soviet Union’s Biopreparat program who later defected to the United States, provides a firsthand account of one of the largest biological weapons programs ever undertaken.

[28] McKinsey & Company, The Emerging Epicenter: Asia’s Role in Biopharma’s Future (2026). McKinsey estimates that Chinese-developed assets now represent roughly 28% of the global innovative clinical pipeline, up substantially from earlier years and indicative of China’s rapidly expanding influence in biopharmaceutical research and development.

[29] PharmaSource, China Biopharma Out-Licensing Surges to Record $137.7B in 2025; 2026 on Pace to Break It Again (2026). Chinese-developed assets represented roughly one-third of global cross-border biopharma licensing deal value in 2025, highlighting China’s emergence as one of the world’s most important sources of new drug innovation.

[30] Arnold & Porter, The BIOSECURE Act Becomes Law in the United States (2025). Enacted as part of the National Defense Authorization Act, the BIOSECURE Act restricts U.S. government relationships with certain foreign biotechnology companies and reflects a broader policy effort to secure biopharmaceutical supply chains, protect sensitive biological data, and strengthen domestic biotechnology capabilities.

[31] Pharmaron, Annual Report 2025; Minzhang Chen, Ph.D., WuXi AppTec Investor Day Presentation (2025); and U.S. Bureau of Labor Statistics, Occupational Employment and Wage Statistics (2023). Together, Pharmaron and WuXi report employing approximately 30,000 chemists, illustrating the extraordinary scale of China’s contract research and development infrastructure and helps explain its cost and capacity advantages in drug discovery and development services.

[32] Internal compensation analysis. We estimate that the fully loaded annual cost of a chemist is approximately $250,000 in the United States versus roughly $90,000 in China, illustrating one source of China’s cost advantage in drug discovery and development.

Obvious Ideas